We are in unprecedented times (Lowest bond yields, highest debt, Crazy P/Es). Back-testing is only so useful. And only 20 years even less. We just had a GDP drop which is the largest since WW2 for some, or since 1929 for the U.S.

Look at Japan's stock market index e.g. for what the future could look like.

Historically low bond yields: The room for rates to go lower is low. I would suggest to be careful with investing in them. If a rate hike comes eventually, both bonds (depending on maturity) and stocks (see december 2019 S&P 500) will fall. With negative real yields (bond yields - inflation), precious metals and related companies are lot more interesting. Perhaps REITs or some blend of solid dividen-paying companies. Anything that is somewhat inflation resistant.

Did you adjust your calculations for inflation?

For the S&P 500, the absolute worst-case is 58 years of not being up, I believe. 1929 - 1987.

Edit: This ignores dividend reinvestment. It seems to be 1929-1944.

I've seen that gap mentioned a few times in this thread. I checked out the visual in the thread [1] and I have a question since time makes everything complicated. This is definitely an example of a worst case scenario, exactly as you mentioned.

How do we calculate that in the total risk assessment? For this outcome to be true, you would have had to invest all of your money in a 6 month period and then tried to exit in a 3 month period during those referenced years.

It would also assume that you are not investing at any other period in between, which is typically advice that goes hand in hand with index funds and tracking the market. In theory and all things being equal, it sounds like that is neutralized if we try to get out in the periods I mentioned above, right? This also assumes no dividends have been paid out.

It seems like the maximum risk is high since the return could be 0% in theory but it also seems like the chance of that happening being _very_ low.

Genuinely curious how you think about it and what else is missing. It definitely makes me want to learn more about how we've stabilized the economy after The Great Depression.

From my point of view, as someone who is invested into an all-world blend like VT or VFFVX, it has been 2.5 years somewhat flat, and we still seem to be at a peak.

https://www.multpl.com/shiller-pe .

I cannot really gauge risk in a systematic like you'd like to.

I'm generally pessimistic, because GDP growth is low, central banks have rates in a choke hold promoting misuse of capital. (In theory many existing companies shouldn't exist. Many are unprofitable, but they get by on cheap loans. Thereby taking away resources/people from potential/future profitable businesses). The ECB couldn't even raise rates in a supposedly economic growth period.

The Fed did in 2019 while reducing the balance sheet, and it ended in a correction and lower rates and a restart of QE.

Low rates also put a lot of pressure on banks and local banks.

Economies and the world are increasingly financialized. The financial market adds little value to the real world aside from "productive" (think GDP-increasing / not consuming) lending.

Consumer loans are awful. Buying your first house/land on a loan is good, though.

Interest payments reduce economic output in the present.

Individuals spend income of the future now, and depress future spending.

E.g. interest payment of the U.S. are ~300bil/year right now ~10% of the budget.

And for many economies and governments there is no end in sight.

Ultimately this can only be solved by reducing spending (which doesn't seem likely for many governments), inflating it away, keeping rates at 0% forever effectively spending printed money, i.e. inflating it away.

Also central banks can buy assets in the open market at face value to lower yields and swallow the coming defaults (which again means inflating it away, and also sending the clear signal that everyone will be bailout, perhaps again in the future).

One aspect of this dynamic is currency demand through e.g. being an important world currency or having export surplus. Some countries can print money better than others.

When I say "inflate" I don't only mean according to CPI. If all the money goes into assets like equities or real estate, it is inflating that.

The stock market feels like a ponzi scheme more than anything.

I'm simplyfing here.

Some countries are better than others.

Perhaps a valid investment strategy would be to invest into indexes of good countries.

That felt a lot like rambling, but I hope you get some value from it.

I'm interested in your thoughts.

I'm guessing you're in the US. I'm sure you can find papers and articles doing back-testing to the 1920s, which would include the Great Depression. If you can wait long enough, things have always recovered and earned a return.

> Did you adjust your calculations for inflation? For the S&P 500, the absolute worst-case is 58 years of not being up, I believe. 1929 - 1987.

Not my calculations. That's also assuming that one has zero bonds: for most people, who are saving for retirement, the component of the portfolio that goes into fixed income rises as age approaches 65. What were bonds during that time?

Most average people don't have the stomach for 'raw' 100% equity holdings, and so bonds are often present; bonds also allow for having 'dry powder' available for rebalancing. Scenarios like these are why portfolio theory can be complicated:

For good layman treatments on the subject I recommend the works of William J. Bernstein, The Intelligent Asset Allocator, The Four Pillars of Investing, and Rational Expectations:

> Historically low bond yields: The room for rates to go lower is low.

One does not necessarily buy bonds for returns, but also (perhaps) to manage volatility (which is often used as a proxy to measure risk). And low bonds are not anything new:

And one has to look at the real return of bonds over the decades: yes nominal numbers are low now and were high in the past, but inflation was high in the past as well (e.g., 1980s).

Both of you make excellent points.

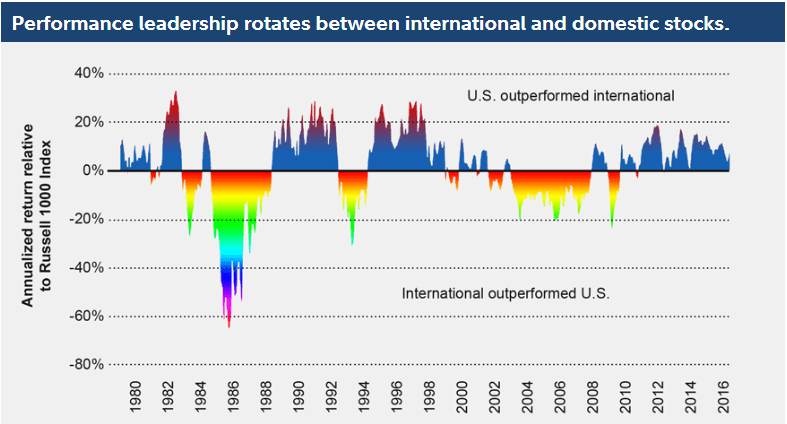

I guess I'm jaded by the fact that VT (or e.g. VFFVX) has been almost flat for 2.5 years now.

A pure US investment would have fared better.

I'm pessimistic about bonds because of the debt bubble (gov debt, MBSs, CLOs, corporate bonds) and low yields.

Governments couldn't stomach higher rates, either.

In the big sell-off we have seen in March everything went down together margin-call style. I guess it did lower volatility, but it also provided little upside.

Euro yields are even negative.

I don't see how any of the countries possible exit strategies could be good for bonds.

> […] almost flat for 2.5 years now. A pure US investment would have fared better.

First: 2.5 years is a ridiculously short investment timeframe. I have sneakers older than that.

Second: perhaps it would have, but there was no way you could have known that ahead of time. Yes, from 2010-2019 the US markets (often measured by the S&P 500) has seen high returns. Now go back to 2000-2009 and see how things faired.

As a Canadian I often see often asking "why invest in Canada at all? why not go all-US?". This is often asked by people younger than 35 or so, who haven't looked up a bit of history, and only know about the last few years (look up the term "recency bias"). There have been times where Canadian equities outperformed the world, and also when international has outperformed the US:

You can make a good decision with the information you have available, but the result still be disappointing. See the video "How to Evaluate Your Investment Decisions":

{kind=link}

Historically low bond yields: The room for rates to go lower is low. I would suggest to be careful with investing in them. If a rate hike comes eventually, both bonds (depending on maturity) and stocks (see december 2019 S&P 500) will fall. With negative real yields (bond yields - inflation), precious metals and related companies are lot more interesting. Perhaps REITs or some blend of solid dividen-paying companies. Anything that is somewhat inflation resistant.

Did you adjust your calculations for inflation? For the S&P 500, the absolute worst-case is 58 years of not being up, I believe. 1929 - 1987. Edit: This ignores dividend reinvestment. It seems to be 1929-1944.